Your cart is currently empty!

Our Prominent Clients

CONCEPT PAPER ON WAREHOUSING

SJES131015 Dated:14th Oct’15

Evolution of Warehousing in India

Until decade ago, warehousing in India was a synonym for basic four-walled structures with sub-optimal sizes, inadequate ventilation & lighting, lack of racking systems, poor hygiene conditions and lack of inventory management or technology solutions such as Warehouse Management System (WMS). Although modern warehouses have begun to develop across India, there is still a significant growth story that remains to be played out in India.

Comparative Analysis of Key Variables in Warehousing Space

| PARAMETERS | INDIA | CHINA | USA |

| Market Maturity (Fragmentation by contribution of key players to the total industry cost) | · Unorganized, fragmented warehousing industry | · Highly fragmented, top 20 companies contribute to 7% of revenue | · 20 largest companies control less than 30% of the market |

| Warehouse Infrastructure:

· Size · Centralization of warehouse · Infrastructure |

· Godowns with approx. size of <10,000 sq.ft

· Multiple warehouses, one in every state · Poor Infrastructure · High pilferage and loss |

· Market is fragmented in terms of operator’s geographical presence

· Average level of Infrastructure with small godowns |

· Warehousing companies operate a single facility of 200,000 sq.ft

· Excellent Infrastructure |

| Value Added Services

|

Poor | Neutral | Good |

| Level of Outsourcing

|

Poor | Poor | Good |

| Skilled Labour

|

· Labour available but with poor training | · Labour available but with poor training | · Highly skilled trained Labour |

| Technology Used

|

Poor | Neutral | Good |

| Consolidation:

Level of usage of Large scale logistics parks & free trade & warehousing zones |

Poor | Neutral | Excellent |

Source: KPMG in Hong Kong Report on Transport in China (2008), Industry discussion

Although large, Most of the warehousing space in India lies with the unorganized players- largely on the domestic side.

Structure of the Indian warehousing Industry (2008)

85% 367 mn sq.ft 8% 36mn sq.ft

433 mn sq.ft

15% 66 mn sq.ft

92% 398 mn sq.ft

Source: KPMG Analysis

The Industry is undergoing a number of supply and demand changes as follows-

- Resurgence of the Indian Economy & Demand-Supply Gap:

After the economic slowdown in 2008-09, India is again witnessing a surge in the need for storage space. According to an estimate, an additional 120 million sq.ft of warehousing space was needed by 2012 to bridge the demand-supply gap (accounting for announced projects), which in turn is a massive investment opportunity for the private sector.

- Implementation of GST:

Owing to multiple & differential state-level taxes, companies in India have set up multiple warehouses, often one per state (to minimize intra-state movements & associated taxation), servicing various parts of the country. This is extremely inefficient & leads to higher unit & inventory carrying costs. Effective April 2016, the govt. of India plans to implement a uniform Goods & Service Tax (GST). As a result there will be a significant re-organization of warehousing space in India. Several leading companies & logistics service providers have already set up these large warehouses, but many are in desperate need of capital and knowhow from foreign investors to capitalize on the opportunity.

- Infrastructure Development:

Development of key infrastructure projects related to ports, highway & rail projects- such as the Golden Quadrilateral (GQ) project, NSEW Project, & Dedicate Freight corridor (DFC) is expected to create new warehousing hubs aligned to these infrastructure points.

- New Storage Models:

Several players in India- such as Multi modal logistics park (MMLP), Mega Food parks (MFP) and Free Trade Warehousing Zones (FTWZs)- have announced next generation storage models.

Emerging Opportunities in India

| STRATEGIC IMPERATIVE | CAPITAL DRIVEN VALUE ADDITION OPPORTUNITIES | EXAMPLE SEGMENTS |

| CREATING NEW SEGMENT | · Bringing in Know-how from overseas markets

· Showcasing Proof of concept to customers & building awareness on the back of a strong global brand |

· 4PL

· Logistics Park · FTWZs · Air Cargo Complex · Shipbuilding & Shipyards |

| GROWING THE SEGMENT | · Introducing processes to enable an efficient scale up

· Developing business plans for expansion · Sensible capital allocation · Providing HR & management bandwidth |

· 3PL

· Modern Warehousing · Project Logistics · Cold Chains |

| CHANGE IN EXISTING & MATURE SEGMENTS | · Improving automation & tech adoption

· Migrating existing services to new industry segments · Access to new geographies or customers · Streamlining operations |

· CFS

· Courier Services · Offshore Logistics · Ports |

| TRANSFORMATION | · Acquisitions of leading market players

· Process improvement · Cost & profitability management · Divestment or asset lightening |

· Freight Forwarding

· FTL Trucking · Shipping · NVOCC |

Impact of Regulatory changes on Warehousing in India:

Warehousing Development & Regulation Act 2007 (WDRA 2007)

Context of Discussions

- Evolution of Warehousing / Storage

- Historical Perspective

- Business perspective

- Current State of Warehousing in India

- Future Trends in Warehousing business

- What is WDRA? Why do we need it?

- What are the impacts of WDRA on Business?

Evolution of Warehousing / Storage

Warehousing – Historical Evolution (Regulatory History)

Historical Perspective

- Public Warehousing in India for Supply Chain Management or Logistics??

- Why Public Warehousing?

- As warehousing needs huge capital investments with low returns, Public warehousing was inevitable

- 1928 Royal Commission on Agriculture recommended establishments of licensed warehouses.

- 1954 All India Rural Credit Survey Committee Reiterated the need for Warehousing in Public Sector

- 1956 Agriculture Produce (Development & Warehousing Corporation) Act, 1956 passed.

Warehousing – Historical Evolution (Regulatory History)

- 1962 Warehousing Corporation Act, 1962 for creation of Warehousing.

- Central & State Warehousing Corporation (CWC & SWCs) were established under this Act

- 2005 WDRA Bill

- 2007 WDRA Act

- Public Sector – More than 2000 Warehouses = 54 million tons

- Total capacity in Private Sector is 300 million tons out of which 8% is in the organized sector.

Gaps that Unorganized Players are incapable of Filling

- More than 80% of the warehouses in and around NCR and 50% in and around Mumbai area are less than 10,000 Sq. ft. in size (AC Nielsen Primary Survey)

- Stock damage in storage is significant cost.

- Poor Storage conditions at the C&F agents

- A variable cost model in warehousing (pay per use) is yet to evolve

- Large Infrastructure Gap

- High Transit Times.

- Low Penetration of IT in Logistic Sector

- Complex Tax Laws and Regulations.

- Lack of Skilled Manpower.

Warehousing in Future – Pointing Trends

- Nascent Food Processing in India – 6.3% of GDP and 13% of Exports

- The Indian food market is estimated at over US$ 182 billion, and accounts for about two thirds of the total Indian retail market.

- The retail food sector in India is likely to grow from around US$ 70 billion in 2008 to US$ 150 billion by 2025 (McKinsey & Co)

Few visible Growth drivers of the Economy

- Growths driven by demographics and population:

- Large population of 1.1bn (UN 2005) : India has a high consumption base.

- 45% under 20 years of age: Large numbers to participate in the creation of wealth.

- Middle class of approx. 340m with increasing spending power.

- Some of the many growing industries:

- Telecommunication: 771m mobile phones (as on Jan’11) as per TRAI

- Automotive: World’s largest motorcycle manufacturer; increased outsourcing of automotive ancillaries to India.

- Drugs and Pharma: 4th largest in the world

- Information Technology: World’s 3rd largest optical media manufacturer; 2nd largest software developers.

- Gems and Jewellery: World’s largest exporter of diamond jewellery

- Sourcing hub of Ready Made Garments

- India is emerging as a potential and important outsourcing / manufacturing hub.

Warehousing – Issues and Challenges

- No adequate warehousing infrastructure.

- Warehousing does not exist as a concept in town planning

- Warehousing adds to the cost, and also increases the touch points that might deteriorate the product.

- Substantially losses to the economy every year due to inadequate Warehousing

Warehousing Development and Regulation Act, 2007

Why WDRA?

What is WDRA?

WDRA 2007 (Warehousing Development Regulation Act 2007)

- An Act enacted by Parliament in the Fifty-eighth Year of the Republic of India to:

- Make provisions for the development and regulation of warehouses,

- Negotiability of warehouse receipts

- WDRA 2007 will lead to:

- standardization of the warehousing activities in the country,

- efficient price discovery for warehoused products,

- use of negotiable warehousing receipts which are fundamental to the competitiveness of the industry.

- Possible inclusion of warehousing in the town planning and thereby availability of land pockets for warehouse development.

- No Distress sales by the farmers

Impact of WDRA – Significance to Farmers

- Avoid Distress Sales by Farmers

- Obtaining of finances against the stored produce

- Higher returns to farmers

- Higher level of protection though enhanced standards of warehousing infrastructure.

- Reduction in losses by adoption of standardized storage practices.

- Enhanced scope for trading through Spot/Future commodity exchanges

- Effective dispute redressal mechanism and quick compensation of loss/damage

- Efficient Supply Chain

- Reduced dependency in Money Lenders.

Impacts of WDRA – Significance to Insurance Cos and Banks

- Enhanced scope for lending due to increased confidence in the system.

- With a legal framework available, Banks / Insurance companies would have an increased role in the warehousing business (especially farm sector) by way of funding individuals/groups.

- Insurance companies would also have increased business opportunities as insurance will be an essential requirement before issuing NWRs due to the liabilities of the warehouseman in the WDR Act.

- With a stable NWR system in place, owners of inventory can borrow foreign currencies for which real interest rates are lower, against inventories of export commodities, thereby hedging against the foreign exchange risk of foreign borrowing. This practice is followed in Kenya and Uganda where coffee stocks are often financed in Pound Sterling.

- Reduction in cost of finance and Risk

Impacts of WDRA – Other Significance

- Reduction in Logistics and Transportation Cost

- Increase in warehousing business by enhanced utilization by the farmers.

- Expansion of the warehousing in rural areas thereby making the facilities more accessible.

- Expansion of cottage industry in rural areas

- Enhancement of employment in the rural areas.

- Stabilizes prices by balancing demand and supply

- Faster delivery system

- Legal Empowerment

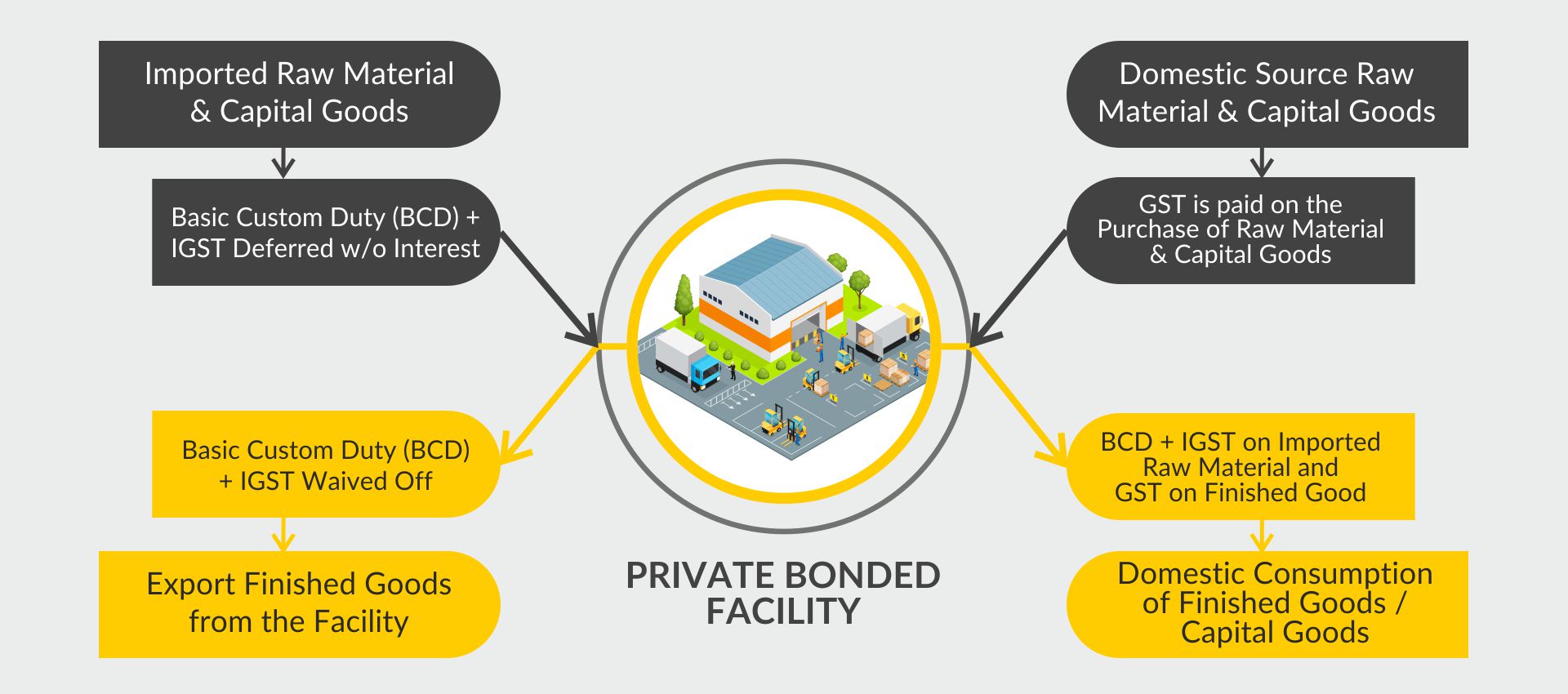

Checklist for Bonded Warehousing Application with Indian Customs:-

- Details of Premises Ownership (Supported by relevant documents)

- Self-assessed declaration about the maximum storage capacity of the warehouse in MT and CBM (Volumes)

- Security Bond equivalent to the applicable Import duty of all the stored goods

- Solvency Certificate from the bank for minimum amount of INR 50 Lakhs

- IEC Code (If available)

- Bank Verified signature

- 5% of the total value of the stored goods as a security deposit with Customs

- NOC from the States Fire Department

- Details of the Civil structure, security arrangements, IT Infrastructure available

Our Role as a Consultant on Warehousing

- To help clients in getting their warehouse registered as a Public bonded warehouse

- To provide consultancy to warehouse owners on operational aspects

- Assist warehouse owners in setting up of the warehouse by arranging a tie-up with the equipment providers, logistics providers, space designers, security services providers etc.

- To assist warehouse owner in integrating their space with the demand segment through analysis of the markets, products, area etc.

- Assistance in integrating the warehousing activity with the nearest Customs port or Railways sidings.

- Consultancy on Marketing & Operational strategy & development, Inter-State Taxation etc.

Prepared By-

Mr. Ravi Shekhar Jha

M/s S.J. EXIM Services

New Delhi

For Further Assistance on Public/Bonded warehousing please contact the undersigned:-

- Ravi Shekhar Jha- +91-9999005379 E-mail: jha.sravi@gmail.com

One response to “Warehousing Industry in India: Private/Public Bonded Warehouse”

-

Reblogged this on S J EXIM Services and commented:

Warehousing in India!!

Hello,

I’m Mimansa

Welcome to SJ EXIM, your corner of the internet dedicated to all things related to Indirect tax I Customs I Arbitration I Insolvency Advisory in India. Let’s craft a solution for you! Connect via email…..

Let’s connect

Follow our Updates/News!

Stay updated & join our newsletter.

Leave a Reply