Legal Paradigm for Export of Paper from India

CONTENTS:

| DESCRIPTION | |

| Introduction SJ EXIM Services | |

| Abbreviations | |

| EXPORTS OVERVIEW FOR PAPER PRODUCTS | |

| REFERENCES-NOTIFICATION/CIRCULAR | |

| EXPORT PROCESS FLOW DIAGRAM | |

| LIST OF DOCUMENTS | |

| Important Extracts of Notifications/Circulars |

YouTube: View Our Introduction on YouTube

About SJ EXIM Services:

Our Expertise: Your partner for Indirect Tax matters & Arbitration

At SJ EXIM Services, we specialize in providing comprehensive solutions at the intersection of tax law and dispute resolution. With a dedicated team of experts, we navigate the complexities of indirect taxation systems worldwide, ensuring compliance and optimizing tax strategies for our clients.

We offer a unique blend of tax advisory services, focusing on indirect taxes such as VAT, GST, customs duties, and excise duties. We assist businesses in understanding their tax obligations, structuring transactions efficiently, and resolving disputes with tax authorities effectively.

In addition to our tax expertise, we have a strong emphasis on arbitration as a preferred method for resolving tax disputes. Our experienced arbitrators guide clients through the arbitration process, offering strategic advice and advocacy to achieve favorable outcomes.

At SJ EXIM Services, we prioritize client satisfaction by delivering tailored solutions that address their specific tax challenges and arbitration needs. With our depth of knowledge and commitment to excellence, we strive to be a trusted partner for businesses seeking expert guidance in navigating the complexities of indirect taxation and dispute resolution.

Our Services:

- Indirect Tax- Customs

- Arbitration

- Foreign Trade Policy-FTP

- Classification Issues & Advisory

- Indirect Tax Solicitation

- Customs and Excise Duty Consulting

- Compliance Review and Audit Support

- Cross-Border Taxation

- Training and Workshops

- Central Licensing

- Pro Bono Consulting

Get in Touch:

Embark on a journey towards enhanced tax efficiency and compliance excellence with SJ EXIM Services. Contact us today to schedule a consultation with our seasoned experts. Let us be your guiding light through the intricate web of indirect taxation & Arbitration, allowing you to focus on what you do best – driving your business forward.

ABBREVIATIONS:

- Indian Rupee: INR

- Export of Goods and Services: EOGS

- Freely Convertible Currency: FCC

- Reserve Bank of India: RBI

- Central Board of Indirect Taxes & Customs: CBIC

- Master Circular: MC

- Notification: Notfn.

- Circular: CIR

- Trade Notice: TN

- Public Notice: PN

- Tariff: (T)

- Non-Tariff: (NT)

- Authorized Dealer: AD

- Harmonized System of Nomenclature: HSN

- Indian Trade Classification (Harmonized System): ITC(HS)

- Shipping Bill: SB

- Let Export Order: LEO

- Bill of Lading: BL

- House Bill of Lading: HBL

- Master Airway Bill: MAWB

- House Airway Bill: HAWB

- Port of Loading: POL

- Port of Discharge: POD

- Invoice: INV

- Packing List: PL

- Certificate of Origin: COO

- Free Trade Agreement: FTA

- Preferential Tariff Agreement: PTA

- Warehouse: WH

- Customs House Agent: CHA

- Customs Broker: CB

- Importer Exporter Code: IEC

- Goods & Service Tax Registration Number: GSTIN

- Authorized Economic Operator: AEO

- Incoterms: INCO

- Letter of Credit: LC

- Cost Insurance Freight: CIF

- Cost & Freight: CFR

- Free on Board: FOB

- Direct Payment: DP

- Advance Payment: AP

- Delivery against Acceptance: DA

- Financial Task Force: FATF

- Discount: Disc

- Manufacturer: Mfr

- Consignee: CNEE

- Unit of Measurement: UOM

- Export Promotion Council: EPC

- Registration cum Membership certificate: RCMC

- Export Data Processing and Monitoring System: EDPMS

- Logistics Service Provider: LSP

Sources: CBIC, RBI, ICEGATE, Govt of India

EXPORTS OVERVIEW FOR PAPER PRODUCTS FROM INDIA

DGFT POLICY

| S NO | ITC(HS) CLASSIFICATION | DESCRIPTION | Export Policy |

| 1 | 4810 9900 | Other-Other paper and paper board | Free. Export Permitted under License for Stock lots |

| 2 | 4811 5190 | Other | Free |

| 3 | 4805 9300 | Other- Weighing 225 g/m or more | Free |

| 4 | 4802 5590 | Other | Free |

| 5 | 4806 2000 | Greaseproof papers | Free |

| 6 | 4805 9100 | Other-Weighing 150 g/m 2 or less | Free |

Source: DGFT

Chapter Notes: Notwithstanding anything contained in Note 12, if paper and paper products of heading 4811, 4816 or 4820 are printed with any character, name, logo, motif or format, they shall remain classified under the respective headings as long as such products are intended to be used for further printing or writing.

Supplementary Notes: For the purposes of sub-headings 4804 11 and 4804 19, Kraft-liner means machine-finished or machine-glazed paper and paperboard, of which not less than 80percent by weight of the total fibre content consists of wood fibre obtained by the chemical sulphate or soda processes, in rolls, weighing more that 115 g/m2 and having a minimum Mullen bursting strength as indicated in the following table or the linearly interpolated or extrapolated equivalent for any other weight.

For the purposes of sub-headings 480421 and 4804 29, sack kraft paper means machine-finished paper, of which note less than 80percent by weight of the total fibre content consists of fibres obtained by the chemical sulphate or soda processes, in rolls, weighing not less than 60 g/m2 but not more than 115 g/m2 and meeting one of the following sets of specifications: (a) Having a Mullen burst index of not less than 3.7 kPa g/m2 and a stretch factor of more than 4.5percent in the cross direction and of more than 2percent in the machine direction.

For the purposes of sub-heading 4805 11, semi-chemical fluting paper means paper, in rolls, of which not less that 65percent by weight of the total fibre content consists of unbleached hardwood fibres obtained by a combination of mechanical and chemical pulping processes, and having a CMT 30 (Corrugated Medium Test with 30 minutes of conditioning) crush resistance exceeding 1.8 newtons/g/m2 at 50percent relative humidity, at 23C.

For the purposes of sub-heading 4805 11, semi-chemical fluting paper means paper, in rolls, of which not less that 65percent by weight of the total fibre content consists of unbleached hardwood fibres obtained by a combination of mechanical and chemical pulping processes, and having a CMT 30 (Corrugated Medium Test with 30 minutes of conditioning) crush resistance exceeding 1.8 newtons/g/m2 at 50percent relative humidity, at 23C.

Sub-heading 4805 24 and 4805 25 cover paper and paperboard made wholly or mainly of pulp of recovered (waste and scrap) paper or paperboard. Testliner may also have a surface layer of dyed paper or of paper made of bleached or unbleached non-recovered pulp. These products have a Mullen burst index of not less than 2kPa.m2/g

For the purposes of sub-heading 4805 30, sulphite wrapping paper means machine-glazed paper, of which more than 40percent by weight of the total fibre content consists of wood fibres obtained by the chemical sulphite process, having an ash content not exceeding 8percent and having a Mullen burst index of not less than 1.47 kPa.m2/g

For the purposes of sub-heading 4810 22, light-weight coated paper means paper, coated on both sides, of total weight not exceeding 72 g/m2, with a coating weight not exceeding 15 g/m2 per side, on a base of which not less that 50percent by weight of the total fibre content consists of wood fibres obtained by a mechanical process.

Export Incentives:

RoDTEP Rate as per Schedule-4R as updated: 1.1% of FOB value per Kg basis. ITC(HS) covered under RoDTEP are 4811 9095 & 4811 9096. Other ITC(HS) mentioned in the above table have been removed from RoDTEP benefit. Please refer to DGFT Notification No 04/2023 dtd 01.05.2023. Link at https://www.dgft.gov.in/CP/?opt=RoDTEP

Exception to the applicability of RoDTEP benefits should be read in context to DGFT Notification no. 19/2015-2020 dtd 17.08.2021.

Duty Drawback Rate as prevailing for ITC(HS) 4802/4805/4806/4810/4811 is 1.2% of FOB value per Kg basis as per Notification No. 77/2023-CUSTOMS (N.T.) dtd 20.10.2023.

REFERENCES-NOTIFICATION/CIRCULAR/PN/TN:

CBIC Notifications/Circulars:

Jawahar Customs SO: Standing Order No. 28 /2005 F. No.: S/12-Gen-418/05 DBK JCH

Public Notice No. 17/2022- Delhi Air Cargo Customs dtd May 2022- Monitoring and realization of export proceeds for shipping bills for which drawback has been claimed and disbursed-reg

CBIC Circular No. 33/2019-Customs dtd 19.09.2019– Clarification regarding duty drawback allowed in cases of short realization of export proceeds due to bank charges deducted by foreign banks

CBIC Circular No. 37/11/2018-GST dtd 15.03.2018- Clarifications on exports related refund issues. Rescinded vide Circular No. 125/44/2019 – GST dated 18.11.2019.

Electronic Duty Credit Ledger Regulations, 2021- Notification No. 75/2021-Customs (N.T.) dtd 23.09.2021– Seeks to notify the Electronic Duty Credit Ledger Regulations, 2021

CBIC Notification No. 76/2021-Customs (N.T.) dtd 23.09.2021-Recovery of Duty credit incase of non-realization of remittance in case of RoDTEP benefits availed

RBI Master Circular:

RBI/2013-14/14: Master Circular No.14/2013-14 as updated on dated 18.06.2014

RBI Notification: Notification No. FEMA 23(R)/2015-RB dtd 12.01.2016-Refer clause no 9(1)(b) & 9(2)(a) & clause 10 for period within which the export documents needs to be submitted

RBI Master Circular: Notification No. FEMA 23(R)/(3)/2020-RB March 31, 2020– Refer clause no 3 vis a vis Notification No. FEMA 23(R)/2015-RB dated January 12, 2016 clause no 9(1)(b)

Notification No. FEMA 23(R)/(1)/2017-RB dtd 23.06.2017- In sub-regulation (C), after the words, “viz. EDF and SOFTEX”, the words “and Exchange Control copies of the shipping bills” shall be deleted.

DGFT Notifications/Circulars:

FTP 2023 Para 2.52, Para 2.53, Para 2.54 read with DGFT Notification No. 43/2015-2020 dtd 09.11.2022.

FCC is covered particularly under para 2.52(a) & 2.52(b) of the FTP 2023.

It is clarified that under FTP Para 1.08– Free passage of Export Consignment Consignments of items meant for exports shall not be withheld/ delayed for any reason by any agency of Central/ State Government. In case of any doubt, the authorities concerned may ask for an undertaking from exporter and release such consignment.

FTP Para 1.09- No seizure of export related Stock No seizure shall be made by any agency so as to disrupt manufacturing activity and delivery schedule of exports. In exceptional cases, the concerned agency may seize the stock on the basis of prima facie evidence of serious irregularity. However, such seizure should be lifted within 7 days unless the irregularities are substantiated.

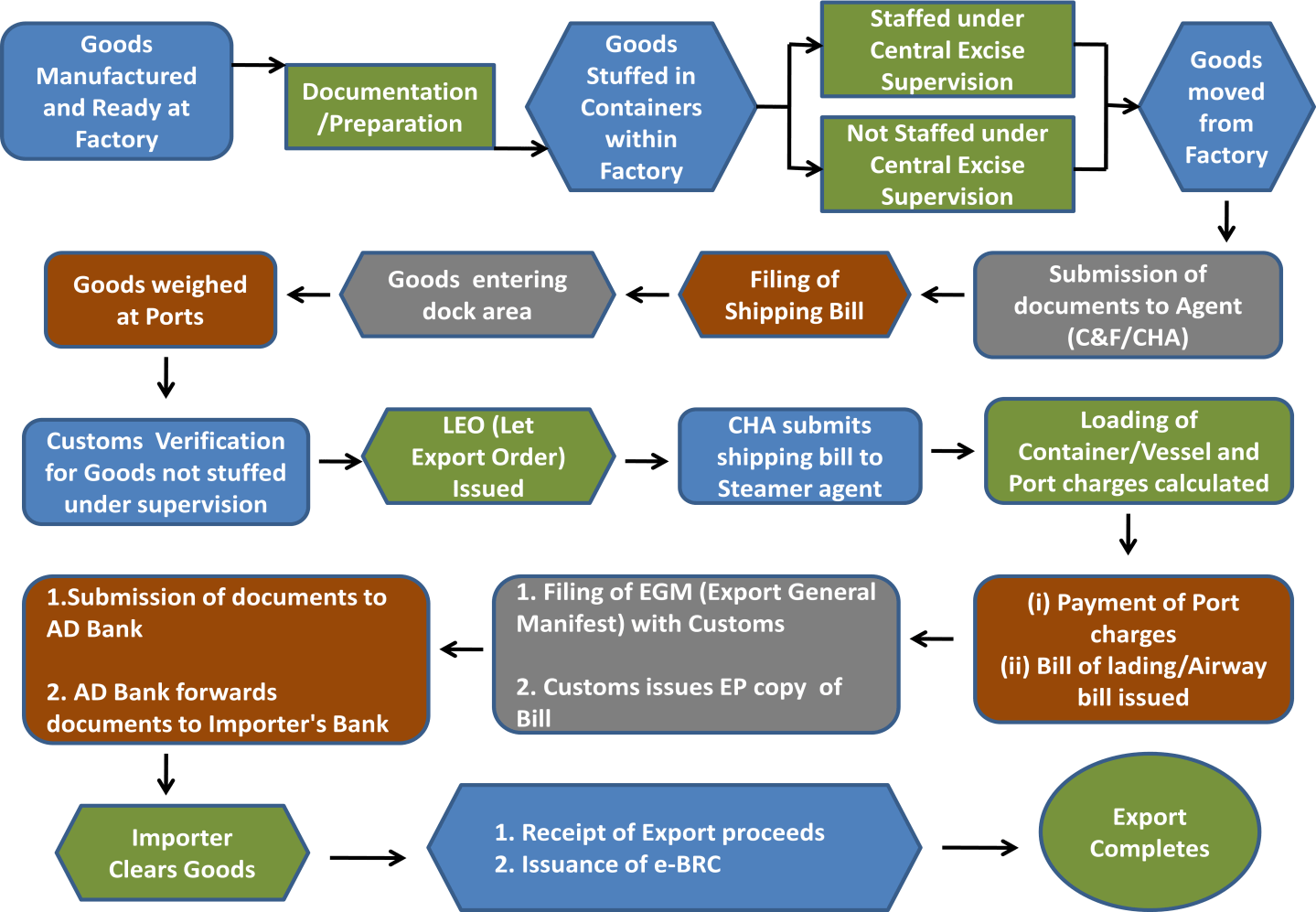

EXPORT PROCESS FLOW DIAGRAM

STEP WISE FLOW AND DOCUMENTS ADDUCED THEREWITH

Goods manufactured & ready at factory

Checklist to move to the next step- Check for the below readiness

- IGST Tax Invoice for Export Invoicing purpose- Section 31 of CGST Act, 2017- against LUT or against payment of IGST is the choice of the manufacturer exporter

- Quality Report/Test report for the manufactured batch of the goods

- Summary & Detailed PL

- Shipping Instruction to the LSP Partner

- Purchase Order from the overseas WH Partner or Subsidiary office/BO

- Agreement copy with the overseas WH Partner or Subsidiary office/BO

- RCMC readiness

- CoO Readiness to be complied at this stage or the CoO must be applied for at this stage

Self Sealing of Goods inside the container

Self-Sealing Permission readiness- Check for CBIC Customs Circular No. 26/2017 dtd 01.07.2017, Circular No. 36/2017 dtd 28.08.2017, Circular No. 37/2017 dtd 20.09.2017, Circular No. 41/2017 dtd 30.10.2017, Circular No. 44/2017 dtd 18.11.2017, Circular No. 51/2017 dtd 21.12.2017

- Exporters who are having Authorized Economic Operator (AEO) status and already availing the self-sealing procedure will have to submit a self-attested copy of AEO registration and self-sealing permission and follow the Radio-frequency identification (RFID) e-Sealing procedure. They are also to be registered with EDI Systems at the FSP section of the customs location at the port of Export

- Exporters who were availing the factory/warehouse stuffing permission under Central Excise supervision would be entitled for self-sealing procedure and would have to follow the RFID e-Sealing procedure and have to register with EDI Systems through Factory Stuffing Permission (FSP) Section of port of export customs.

Goods moved from factory to Port of export

Checklist for this stage:

- IGST Tax Invoice- u/s 31 of the CGST Act, 2017

- E-way bill- u/s 68 of the CGST Act, 2017 read with Rule 138 of the rules framed thereunder

- Export Invoice

- Summary & Detailed PL

- Carting Order/Delivery Order issued by the Shipping Line (S/L) for inward movement of goods inside the port of export, as the case maybe

- Quality/Test Report-Batch test report

- Shipping Instruction to the LSP Partner

- Purchase Order from the overseas WH Partner or Subsidiary office/BO

- Agreement copy with the overseas WH Partner or Subsidiary office/BO

- RCMC copy

- CoO as per DGFT/REX system **

- General KYC or e-KYC as the CB may ask

** Certification of origin of goods with statements on origin

The rules for determining the origin of goods in the GSP scheme of the EU remain unchanged with the application of the REX system. Only the method to certify the origin of goods is changed.

To be entitled to make out a statement on origin, an economic operator needs to be registered in the REX system and to have a valid registration, i.e. a registration which is not revoked. It is however allowed that unregistered exporters make out statements on origin for consignments of originating goods having a value which is below 6 000 EUR.

A statement on origin is a declaration of origin added by the registered exporter on an invoice, a delivery note, a packing list, or any other commercial document allowing to identify the goods and the exporter. The text of the statement on origin is laid down in Annex 22-07 of Regulation (EU) 2015/2447. For the rules concerning the statement on origin, please refer mainly to Article 92 and Article 93 of that regulation.

Filing of Shipping Bill

Checklist for this stage:

- Approved SB checklist & SB No & Date- Ensure that the SB is filed under Consignment basis only- u/s 50 of the Indian Customs Act, 1962 is a statutory provision for entry of goods for exportation.

- EGM Filing- u/s 41 of the Customs Act, 1962 filed by the S/L

- Assessment & Export clearance up to LEO stage u/s 51 of the Indian Customs Act, 1962

- SB submitted to the S/L by the CB for BL finalization & issuance- Check for the Draft BL to get the Final MBL at this stage issued by the S/L or the Carrier

- EP copy is issued by the Indian Customs after SB is given the Let Export Order (LEO)

Submission to the AD Bank by Exporter

Checklist for this stage:

- Exch. control copy/EDF in the form of SB transmitted by ICEGATE system to EDPMS & GSTIN server electronically- No manual intervention is required at this stage

- Exporters copy (EP) along with other shipping documents and PO issued by the overseas partner along with the MSA agreement with the overseas partner to be submitted with the AD bank- Follow the instructions as per the RBI Notification No. FEMA 23(R)/2015-RB dtd 12.01.2016. Kindly Refer clause no 9(1)(b) & 9(2)(a) & clause 10 particularly

- Notification No. FEMA 23(R)/2015-RB dtd 12.01.2016 applies in the above case read with Notification No. FEMA 23(R)/(3)/2020-RB dtd 31.03.2020

Remittance Receipts/e-BRC/Closure at EDPMS

Checklist for this stage:

- E-BRC as issued by the AD bank & updated in the DGFT e-BRC system – Refer to DGFT Notfn No.

- Differential in actual remittances needs to be supported with documentary evidence I order to comply with RBI Master Circular

Reference Para 1.07 of the Foreign Trade Policy, it is a commitment of this directorate to facilitate exports and imports, with a focus on efficient, transparent, and accountable delivery systems. To further improve trade facilitation for exporters, this directorate has implemented an enhanced electronic Bank Realisation Certificate (eBRC) system. This more streamlined process is based on electronic Inward Remittance Messages (IRMs) to be transmitted directly by banks to DGFT. Based on the IRMs received, the exporters shall self-certify their eBRCs.

Exporter is requested to refer to Trade Notice 33 / 2023-24 dated 10th November 2023.

Services provided under the new eBRC system shall include the following.

- IRM / ORM Repository – Search and view the inward and outward remittances uploaded by banks against your PAN. Outward remittances are auto linked to the reference inward remittances.

- Generate eBRC – Self-Certify and generate eBRC against one / multiple inward remittances from bank as per the self-certification criteria.

- View / Cancel eBRC – Search and view the eBRC from Bills Repository. You can also cancel any unutilized self-certified eBRC from here.

- View IRM Utilization Report – Request and download the utilization report for inward remittances and their linkage to corresponding shipping bill/ invoices and eBRC.

GENERIC LIST OF DOCUMENTS REQUIRED FOR EXPORT MOVEMENT:

PRE-SHIPMENT DOCUMENTS: –

- Local GST Tax Invoice for movement from Warehouse/Factory to the port of Export in India

- Packing List

- Certificate of Origin

- Quality Certificate /Testing Certificate issued by the manufacturer

FOR CUSTOMS CLEARANCE: –

- Export Invoice for WH in Italy where the WH player is the CNEE cum Buyer

- PL- Summary & Detailed

- CoO

- Quality Certificate/Test report

- Copy of Agreement with B2B/B2C Buyer, as the case maybe

- SB Checklist duly approved by the Manufacturer cum Exporter

- Shipping bill to be filed on consignment basis- 15 months remittance timeline as per FEMA

- RCMC of CAPEXIL (EPC)

- MBL/HBL/MAWB/HAWB, as the case maybe

FOR AD DEALER BANK FOR EDPMS CLOSURE:

- Final Invoice where the WH Player is the CNEE & end buyer is the actual Buyer-must directly relate to the previous Export Invoice Number & date

- PL- Summary & Detailed

- CoO

- Quality Certificate/Test report

- Copy of Agreement with B2B/B2C Buyer, as the case maybe

- SB Checklist duly approved by the Manufacturer cum Exporter

- Shipping bill to be filed on consignment basis- 15 months remittance timeline as per FEMA

- RCMC of CAPEXIL (EPC)

- MBL/HBL/MAWB/HAWB, as the case maybe

- e-BRC

- Tax Invoice Raised by the WH Player to the Indian Manufacturer exporter showing the deductions/debit for expenses borne by them in Italy & the agreed Fee

CHECKING THE EDPMS STATUS IN ICEGATE

Document as per the attached sample- Live view Link is given below

SAMPLE SB CHECKLIST FOR EXPORT

FORMAT OF EXPORT INVOICE & SB LEO Copy

- Kindly refer to Customs Notification No. 60 /2017-Customs (N.T.) dtd 29th June 2017.

Important Extracts of Notifications/Circulars/FTP/RBI:

- RBI has clarified that such deductions are enabled under notification No. FEMA 23(R)2015-RB dealing with Foreign Exchange Management (Export of Goods and Services) Regulations 2015. In respect of various export promotion schemes, para 2.52 of FTP 2015-20 also states that free foreign exchange remitted by buyer after deduction of bank service charges are taken as export realization under export promotion schemes of FTP. Earlier also, in respect of agency commission paid to agents abroad for securing export contracts, Board vide Circular No. 64/2003-Customs dated 21.07.2003 has allowed such commission up to the limit of 12.5% of FoB value to be considered for payment of duty drawback without deducting it from FoB value in line with the RBI’s Circular No.AD (MA Service) 17, dated 19.5.1999and DGFT’s Policy Circular No. 55 (RE-98) dated 10.02.1998.

- RBI has notified the Foreign Exchange Management (Exports of Goods and Services) Regulations, 2015 for EoGS. These Regulations have been notified through Notification No. FEMA 23(R)/2015-RB dated January 12, 2016 also amended from time to time.

- 100% payments against the EoGS are to be received through the banks in accordance to the manner as specified in the Foreign Exchange Management (Manner of Receipt & Payment) Regulations, 2000 as notified through Notification No. FEMA.14/2000-RB dated May 3, 2000.

- Banks are permitted to allow the exporters to grant trade related loans or advances to the buyers out of the EEFC account without any monetary limit subject to satisfactions of the terms and conditions as notified through Notification No. FEMA 3/2000-RB dated May 3, 2000 as amended from time to time.

- In order to take an extension for a delayed remittance period the Exporter must apply to their bankers through the ETX form issued by RBI or the AD Dealer’s format, as the case maybe.

Valuation under Indian Customs: CVR Rules, 2007

3. Determination of the method of valuation. –

(1) Subject to rule 8, the value of export goods shall be the transaction value.

(2) The transaction value shall be accepted even where the buyer and seller are related, provided that the relationship has not influenced the price.

(3) If the value cannot be determined under the provisions of sub-rule (1) and sub-rule (2), the value shall be determined by proceeding sequentially through rules 4 to 6.

4. Determination of export value by comparison

(1) The value of the export goods shall be based on the transaction value of goods of like kind and quality exported at or about the same time to other buyers in the same destination country of importation or in its absence another destination country of importation adjusted in accordance with the provisions of sub-rule (2).

(2) In determining the value of export goods under sub-rule (1), the proper officer shall make such adjustments as appear to him reasonable, taking into consideration the relevant factors, including-

(i) difference in the dates of exportation,

(ii) difference in commercial levels and quantity levels,

(iii) difference in composition, quality and design between the goods to be assessed and the goods with which they are being compared,

(iv) difference in domestic freight and insurance charges depending on the place of exportation.

8. Rejection of declared value.-

(1) When the proper officer has reason to doubt the truth or accuracy of the value declared in relation to any export goods, he may ask the exporter of such goods to furnish further information including documents or other evidence and if, after receiving such further information, or in the absence of a response of such exporter, the proper officer still has reasonable doubt about the truth or accuracy of the value so declared, the transaction value shall be deemed to have not been determined in accordance with sub-rule (1) of rule 3.

2) At the request of an exporter, the proper officer shall intimate the exporter in writing the ground for doubting the truth or accuracy of the value declared in relation to the export goods by such exporter and provide a reasonable opportunity of being heard, before taking a final decision under sub-rule (1).

Explanation. – (1) For the removal of doubts, it is hereby declared that-

(i) This rule by itself does not provide a method for determination of value, it provides a mechanism and procedure for rejection of declared value in cases where there is reasonable doubt that the declared value does not represent the transaction value; where the declared value is rejected, the value shall be determined by proceeding sequentially in accordance with rules 4 to 6.

(ii) The declared value shall be accepted where the proper officer is satisfied about the truth or accuracy of the declared value after the said enquiry in consultation with the exporter.

(iii) The proper officer shall have the powers to raise doubts on the declared value based on certain reasons which may include –

(a) the significant variation in value at which goods of like kind and quality exported at or about the same time in comparable quantities in a comparable commercial transaction were assessed.

(b) the significantly higher value compared to the market value of goods of like kind and quality at the time of export.

(c) the misdeclaration of goods in parameters such as description, quality, quantity, year of manufacture or production.

Conciliation for Invoicing & Remittance Purposes Key Points for EDPMS Closure:

- Entire set of documents needs to be mapped against the Master Service Agreement/Contract (MSA) between the Indian Exporter & the Overse3as WH Player or the Branch office (BO).- MSA Agreement No needs to be entered into the ERP/SAP as the case maybe and all subsequent documents needs to be mapped to the said agreement number. All commercial Invoices/Tax Invoices/Export Invoices must possess this particular agreement reference no and date.

- Three (3) different set of Invoices needs to be maintained for each transaction/order against the MSA agreement no in the ERP/SAP system, out of which only the local invoice from India Factory/WH to Port of export shall be in INR the rest 2 sets for Export Invoicing & final customers Invoicing needs to be in EURO or FCC as the case maybe.

- Invoice Set 1: Indian Exporter Factory to Port of Export GST Tax Invoice- Must have the MSA agreement no & date as reference.

- Invoice Set 2: Commercial Invoice for Export where the Indian Manufacturer is the Exporter/Shipper, The WH Partner outside India is the Consignee (CNEE) & Notify Party only- Must have the MSA agreement no & date as reference. The value & date on Invoice Set 1 & Invoice Set 2 must be the same in order to avoid any discrepancies in availing the IGST refunds, in case of IGST Paid Tax Invoices.

- Invoice Set 3: Once the Order is triggered on the online e-Commerce portal then a final set of Invoice must be triggered by the Exporters ERP/SAP/CRM which will be having the MSA agreement no & date as reference plus the Reference of Invoice Set 2 to establish the correlation.

- The AD Bank must be provided with the MSA copy, all 3 different Invoices sets as per above along with the SB Leo Copy (Exporters Copy), MBL/HBL (Sea Cargo), CoO, and any other shipping documents that was filed in the e-Sanchit module of ICEGATE EDI system for exports purposes. This exercise has to be done every time there is an export movement.

- A detailed data along with all the supporting documents, conciliation statement of all the outward/inward remittance, eBRCs needs to be maintained for appropriate justification as and when asked by Customs or RBI or the Exporters AD Bank.

- Opening or Hiring of the Warehouses outside India under RBI Approval

AD Banks are permitted to consider the applications as received from the exporters to grant the permissions for opening or hiring warehouses outside India after satisfaction of the certain terms and conditions:

- Exporters’ export outstanding is not exceeding 5% of the exports as made during the previous financial year.

- Exporters’ have a minimum exports turnover USD 1 lac during the previous financial year.

- Exporters are required to obtain the remittance from outside India within maximum 1 year.

- Exporters are required to route the all transactions with the same banks.

- Exporters are initially permitted for maximum 1 year and thereafter renewals are permitted after satisfaction of above mentioned terms and conditions.

- 1st Extension of Time by Banks

- Generally RBI has permitted the banks to extend the period of realization of exports proceeds beyond maximum 180 days 1st time subject to satisfaction of certain terms and conditions:

- Where the exports transactions are not under investigations by the Enforcement Directorate (ED),

Central Bureau of Investigation (CBI) or any other investigation agency

- Where banks are satisfied that the exporters have been unable to realize the exports proceeds beyond the reasons in their control.

- Where exporters have already submitted the declaration that the exports proceeds are to be realized during the extended period.

- Where total outstanding of the exporters are not exceeding 10% of the average exports realizations during the preceding 3 financial years or not exceeding USD 1 million whichever is higher.

- Banks are required to report in XOS statement where outstanding are exceeding 6 months + the extension of time as granted by the banks.

- Banks are permitted to allow extension of time where the exporters have already been filed the court suits outside India against the buyers beside any quantum of outstanding.

- 2nd Extension of Time by Banks

- Banks are permitted to permit 2nd extension of time after obtaining prior approval of the RBI through regional office where the exporters have not been able to realize the exports proceeds for the reasons beyond their controls within the time allowed in 1st extension

- Banks are required to ensure that necessary applications should be filed in duplicate with the RBI through regional office.

- Write off of exports bills by exporters

- (a) Exporters are permitted to self write off or to approach the banks along with shipping documents and appropriate supporting documentary evidences where exporters are not able to realize the outstanding exports dues despite their best human efforts

(b) Banks are permitted to allow write off where exporters have already been surrender the exports incentives and also subject to satisfactions of the certain terms and conditions as notified vide A.P. (DIR Series) Circular No. 03 dated July 22nd 2010:

(ba) Self write off by the ordinary exporters are not permitted where self write off are exceeding 5% of the total exports proceeds realized during the previous calendar year

(bb) Self write off by the Star holder exporters are not permitted where self write off are exceeding 10% of the total exports proceeds realized during the previous calendar year

(bc) Write off by the banks are not permitted where self write off are exceeding 10% of the total exports proceeds realized during the previous calendar year

- Above mentioned limits for the write off are cumulatively available in a calendar year

- Above mentioned limits for the write off is permitted where outstanding is minimum for 1 year + exporters have submitted satisfactory documentary evidences for the best human possible efforts of the exporters having made all efforts to realize the dues and also subject to following circumstances:

- Where the buyers have already been declared as insolvent and a certificate from the official liquidator indicating that there is no possibility of recovery of exports proceeds have also been produced

- Where the buyers are not traceable over a reasonably long time tracking.

- Where the exported goods have already been auctioned or destroyed by the Port, Customs or Health authorities outside India.

- Where the unrealized amounts are representing the balances due in the cases which were through the intervention of the Indian Embassy, Foreign Chamber of Commerce or similar Organizations

- Where unrealized amounts are representing the balance undrawn of the exports bill not exceeding 10% of the invoice value + unrealized amounts are outstanding despite the all best human efforts as made by the exporters.

- (fa) Where cost of resorting to the legal actions are likely to be disproportionate to the unrealized amount

or

(fb) Where the exporters are not able to execute the court degree against the buyer due to reasons beyond their human control.

- (ga) Where bills were drawn for the differences between the value of LC and value of actual exports or differences between the provisional and the actual freight charges

and

(gb) Where the amounts which have remained unrealized due to dishonor of the bills by the buyers + no prospects of the realization.

- Banks are permitted to allow the write off of unrealized outstanding balance after obtaining the evidences from the exporters for surrender of proportionate exports incentives where surrender of proportionate exports incentives are not covered under the A. P. (DIR. Series) Circular No. 03 dated July 22, 2010.

- Exporters are required to submit to the banks the certificates as obtain from the practicing Chartered Accountants (CA) Firms in India indicating the following information’s:

- Exports realization in the preceding calendar year

- Amount of write-off already availed of during the year if any

- Relevant EDF to be written off

- Bill No

- Invoice value

- Commodity exported

- Country of export

- Surrendered proportionate exports benefits as availed by the exporters.

- Write off not permitted

- Where the exports were made to the countries with the externalization problems like the buyers have deposited the value of exports in the local currency + banks outside India have not been allowed to repatriate by the central banking authorities of the country.

- Where the EDFs are under the investigation for the civil or criminal suits by the agencies like: (ba) Enforcement Directorate (ED) (bb) Directorate of Revenue Intelligence (DRI) (bc) Central Bureau of Investigation (CBI) etc.

- Banks are required to report write off of exports bills through EDPMS to the RBI.

- Banks are advised to put in place a systems for their internal inspectors or the auditors including the external auditors as appointed by the banks to carry out the random sample check or percentage check of the write-off against outstanding exports bills.

Banks are required to refer the cases to the RBI through regional office where the cases are not covered under the above mentioned instructions or exceeding the limits as prescribed.

In case you face any issues related to Indirect Tax-Customs, GST, Foreign Trade Policy (FTP), Arbitration matters and Central Licensing and related advisory matters in India then please feel free to get in touch with SJ EXIM Services. We offer Legal advice and litigation support in matters related to Indirect Tax-Customs, FTP, other Indirect Tax matters & Arbitration law, all sorts of Central licensing and related matters. Come and explore the new way of doing business with us!

Connect with us-

@ Team S J EXIM SERVICES, New Delhi, IN

CP: Ms. Shubhra Jha

Web: www.sjexim.services

Tel: +91-9999005693

Email: operations@sjexim.services | shubhra@sjexim.services

YouTube: View Our Introduction on YouTube

Your Partners for “Indirect Tax & Arbitration” in India

Disclaimer:

1. The views are of the Author based on his/her interpretation of the relevant information/documents, applicable law, and government policy and there is no assurance that a court or tribunal or regulatory body or other governmental authority may not interpret it differently.

2. We are not responsible for updating or revising this article on account of any change in law or interpretation thereof or a change in events or circumstances informed or occurring after the date of this article unless specifically requested for it.

3. Our advice should not be taken or used out of context or reproduced for any other purpose or transaction. Views expressed in this update are strictly personal, based on our understanding of the underlying law. We are not responsible for any injury, loss or cost arising to any person who refers to this update and acts or refrains from any act accordingly. We would suggest that detailed legal advice must be sought before relying on this update.

NOTE: All Inquiries/Pro Bono Consulting/Assignments are solicited via email only & it is a PAID Service only!

#CBIC #FEMA #RBI #Export #India #Law #Regulations #Compliance #IndirectTax #IndianCustomsAtWork #ProcessImporovement #LegalBlogs #Icegate #eSanchit #ADBank #BankingRules #Deloitte #KPMG #GrantThornton #PwC #ErnstandYoung #Bainandcompany #McKinsey #BostonConsulting #BCG

Leave a Reply